What Is a Debt Consolidation Loan?

Estimated reading time: 6 minutes

Last updated on November 26th, 2025 at 05:23 pm

A debt consolidation loan is a type of borrowing that lets you combine multiple debts into one manageable monthly repayment.

Instead of paying several lenders at different rates, you take out a single loan to clear them all, leaving you with one fixed payment and one interest rate to deal with.

It’s a common option for people juggling credit cards, overdrafts, or personal loans who want to simplify their finances and potentially reduce what they pay in interest overall. Reports show that the average Briton saves around £1,257 in interest by using a consolidation loan.

Debt consolidation can be done through a secured or unsecured loan, depending on your credit history and whether you have assets such as a home.

The main advantage is that you are able to clear multiple debts at once and save on the interest that might accrue over time by paying them all off early.

You can use a debt consolidation loan at any time, but it is common for people that are remortgaging or getting a new mortgage. It also looks better on your application for a mortgage if you do not have lots of loans and credit open.

How Does Debt Consolidation Work?

Debt consolidation works by using a new loan to pay off your existing debts, leaving you with just one repayment to manage. This can make budgeting easier and may lower your overall monthly cost if the new loan has a lower interest rate than the debts it replaces.

There are two main types of debt consolidation loans:

- Secured loans – These are often tied to your home (sometimes called homeowner loans). Because they use property as security, they usually offer lower interest rates, but missing payments could put your home at risk.

- Unsecured or personal loans – These don’t require property as collateral but often come with higher interest rates, especially if your credit score isn’t strong.

Debt consolidation loans can be offered by banks, credit unions, building societies, and specialist lenders. Some mortgage lenders also offer consolidation products that let you roll unsecured debts into your mortgage balance, though this can extend the repayment period significantly.

See also how unsecured loans work.

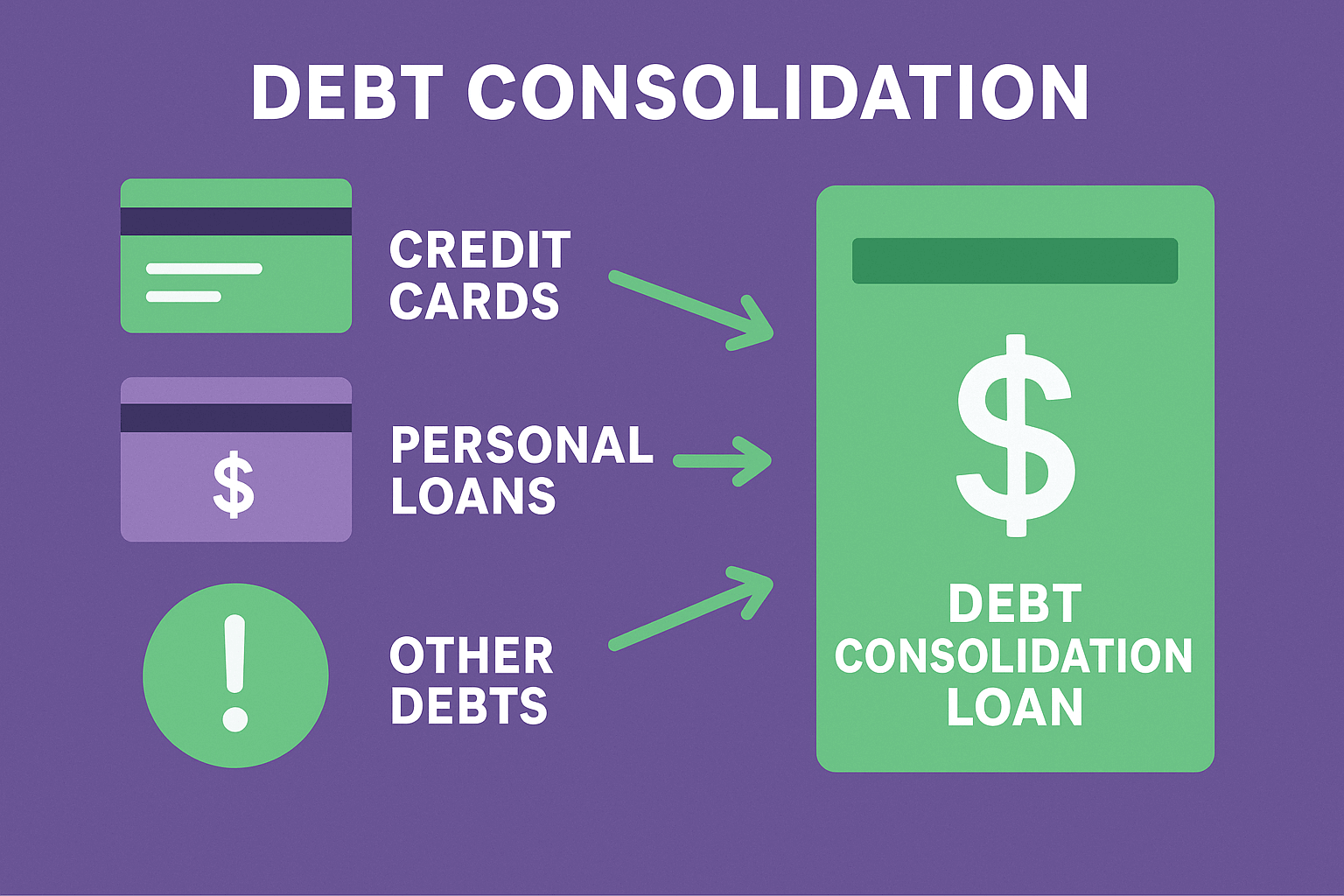

What Debts Can You Consolidate Into a Loan?

You can usually consolidate most types of unsecured debts, including:

- Credit cards

- Personal loans

- Overdrafts

- Store cards

- Catalogue debts

- Payday loans

- Buy now, pay later balances

Secured debts such as mortgages or car finance generally can’t be consolidated through a standard personal loan, unless you choose to remortgage or use a secured homeowner loan.

What Are The Benefits Of Using A Debt Consolidation Loan?

The main benefit of a debt consolidation loan is simplicity: you replace several repayments with one predictable monthly payment.

It can also make your total debt cheaper, if the new loan’s interest rate is lower than the combined cost of your previous debts.

Other potential benefits include:

- Easier budgeting with a single repayment date

- Reduced total interest if the new loan rate is lower

- Possible improvement in credit management by avoiding missed payments

- Less stress from juggling multiple creditors

However, the key is discipline: consolidation doesn’t erase debt, it just restructures it. You still need to manage spending carefully to avoid building up new balances alongside your consolidation loan.

Is It A Good Idea To Use A Debt Consolidation Loan?

Debt consolidation can be a good idea if it genuinely reduces your interest costs and makes repayments easier to manage. But to know whether it helps, you need to compare the total cost, not just the monthly payment.

For example:

- If you owe £10,000 across three credit cards at 25% APR and only make minimum payments, you could pay more than £4,000 in interest over several years.

- If you consolidate that £10,000 into a five-year personal loan at 10% APR, your monthly payment might be around £212, with a total repayment of roughly £12,720 — saving you over £1,000 in interest and clearing your debt faster.

This shows how a lower rate and fixed term can make repayment more predictable and cost-effective. However, if you extend the term too long or don’t change your spending habits, you could end up paying more overall.

What Happens If You Do Not Consolidate Your Debts?

If you don’t consolidate your debts, you’ll continue managing multiple accounts, payments, and interest rates. This can make it harder to keep track of due dates and may increase the risk of missed payments or additional interest charges.

Without consolidation, more of your money may go toward paying interest instead of reducing your balances. Over time, this can keep you trapped in a cycle of minimum payments — especially with high-interest credit cards and overdrafts.

That said, consolidation isn’t the only option. Some people prefer to focus on a debt snowball or avalanche method (paying off the smallest or highest-interest debts first), which doesn’t involve taking out new credit. It depends on your situation, discipline, and ability to qualify for a consolidation loan.

Is Debt Consolidation Good For Your Credit Score?

Debt consolidation can help your credit score in the long run, but only if it’s managed responsibly. In the short term, applying for a new loan may cause a small temporary dip because of the hard credit check. However, once your old debts are paid off and you make regular payments on the new loan, your credit score can gradually improve.

This is because you’ll have fewer active credit accounts, a better debt-to-income ratio, and a clear record of on-time payments. The key is to avoid running up new debts after consolidating, otherwise, you’ll end up owing more and risk damaging your credit profile further.

Debt consolidation loans can be a smart way to simplify your finances and save money on interest, but only if used carefully. Always compare the total repayment cost, check the terms, and make sure the new loan genuinely improves your situation. If you’re struggling to manage debt, it’s also worth speaking to a free, regulated debt advice service before committing to a new credit agreement.

Leave a Reply

Want to join the discussion?Feel free to contribute!